The Business Case: Tapping into an $8tn Opportunity

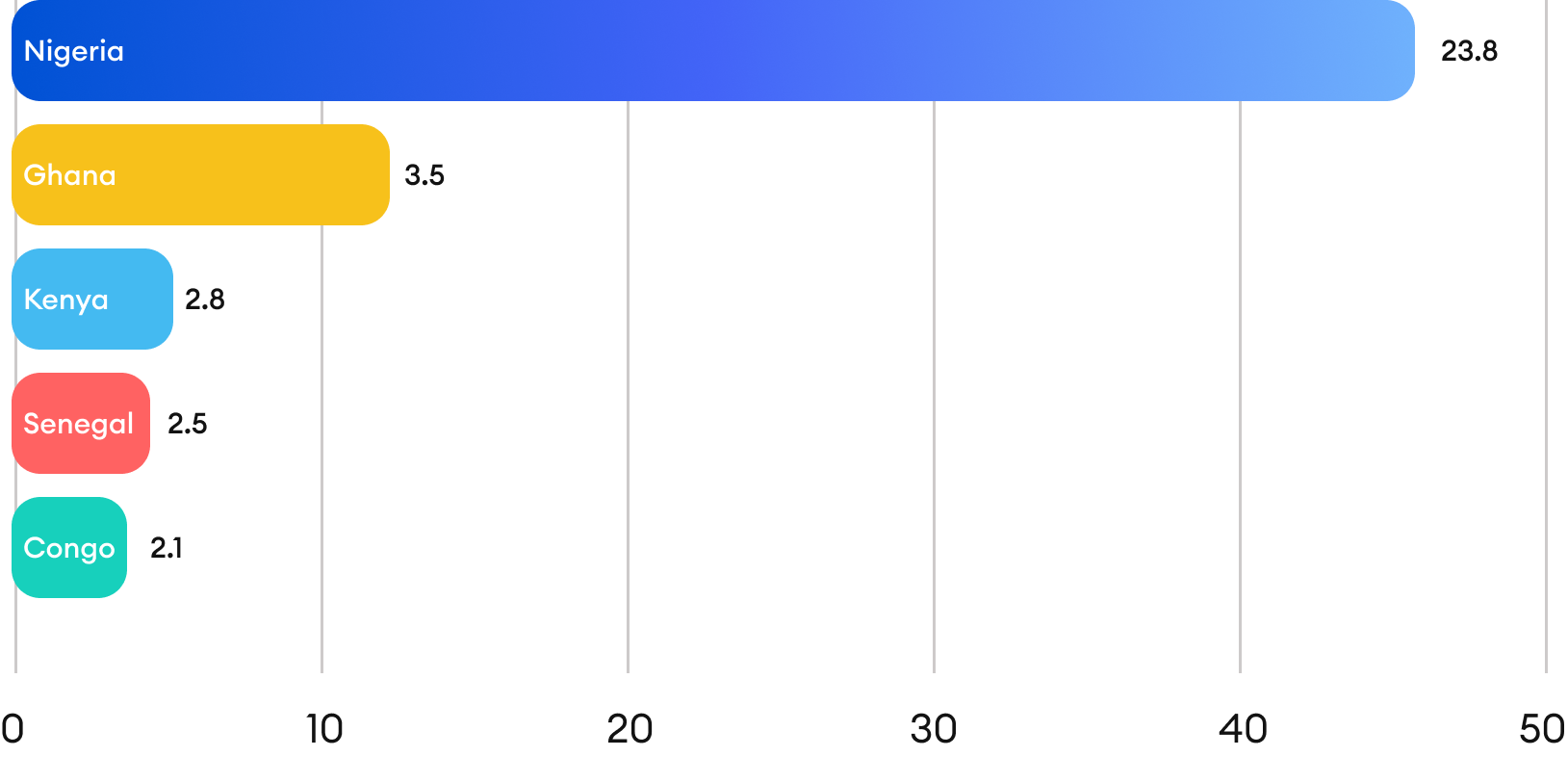

My research synthesized the vast potential of the African growing economy, where a tech-savvy population of over 1.2 billion is currently underserved by traditional banking. By mapping the $45.6 billion in total transactions across our top target markets were Nigeria, Ghana, and Kenya. I identified a massive secondary market in crypto-remittance.

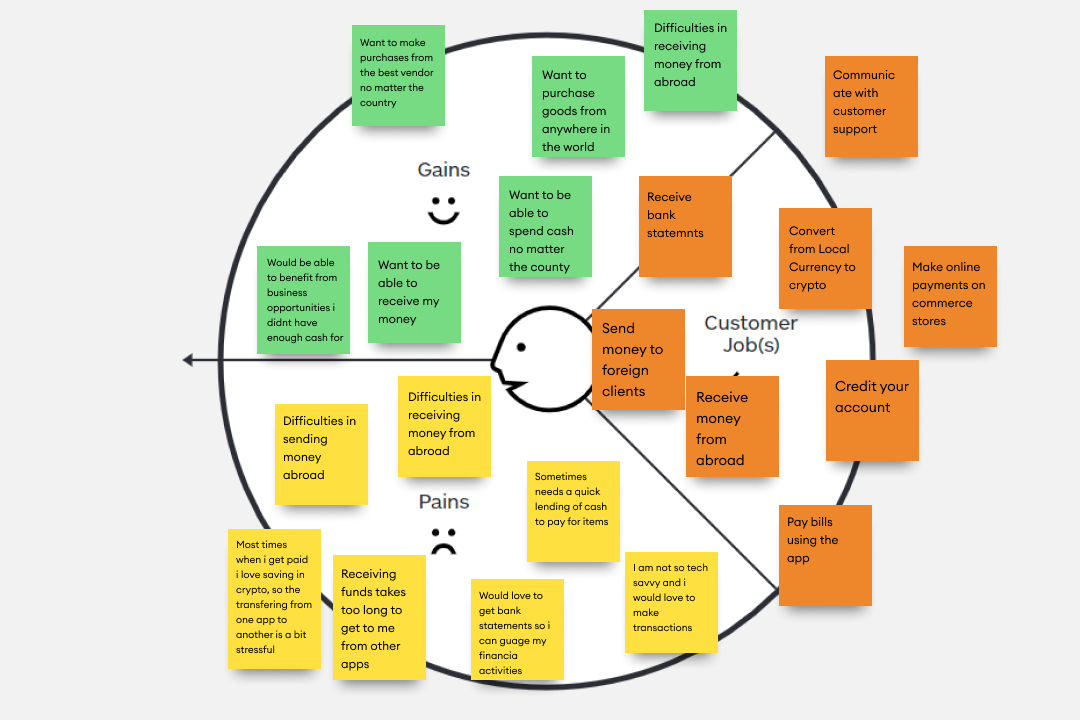

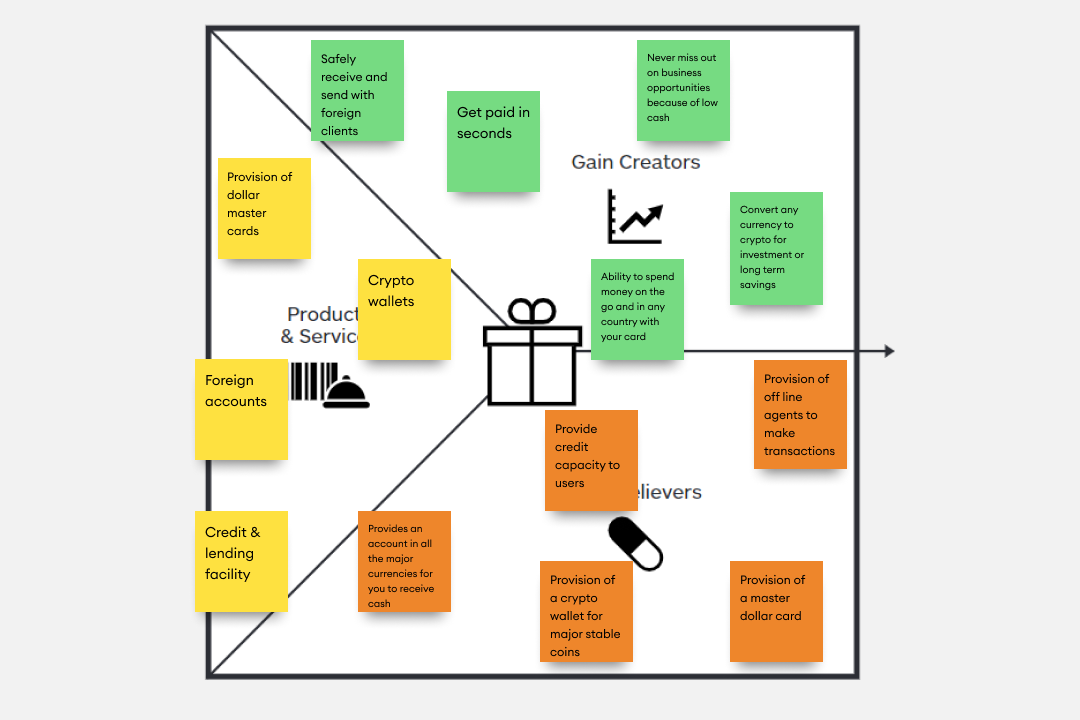

Retailers, Individuals & MSMEs want more. The majority of consumers are underserved.

They need cheaper services.

An improved user experience.

An advanced product value proposition.

45.6 Billion in total transactions in Africa

Our first targets would be the top 5 countries with the highest remittance valueNigeria, Kenya and Ghana.

With the pain points of users requesting payment in crypto currency, it opens up a new market to explore and that would mean another fast growing resource to tap into

Estimated transaction volume of $8tn in 2025

With 10% of this transaction relating with the African market, the opportunities available are endless