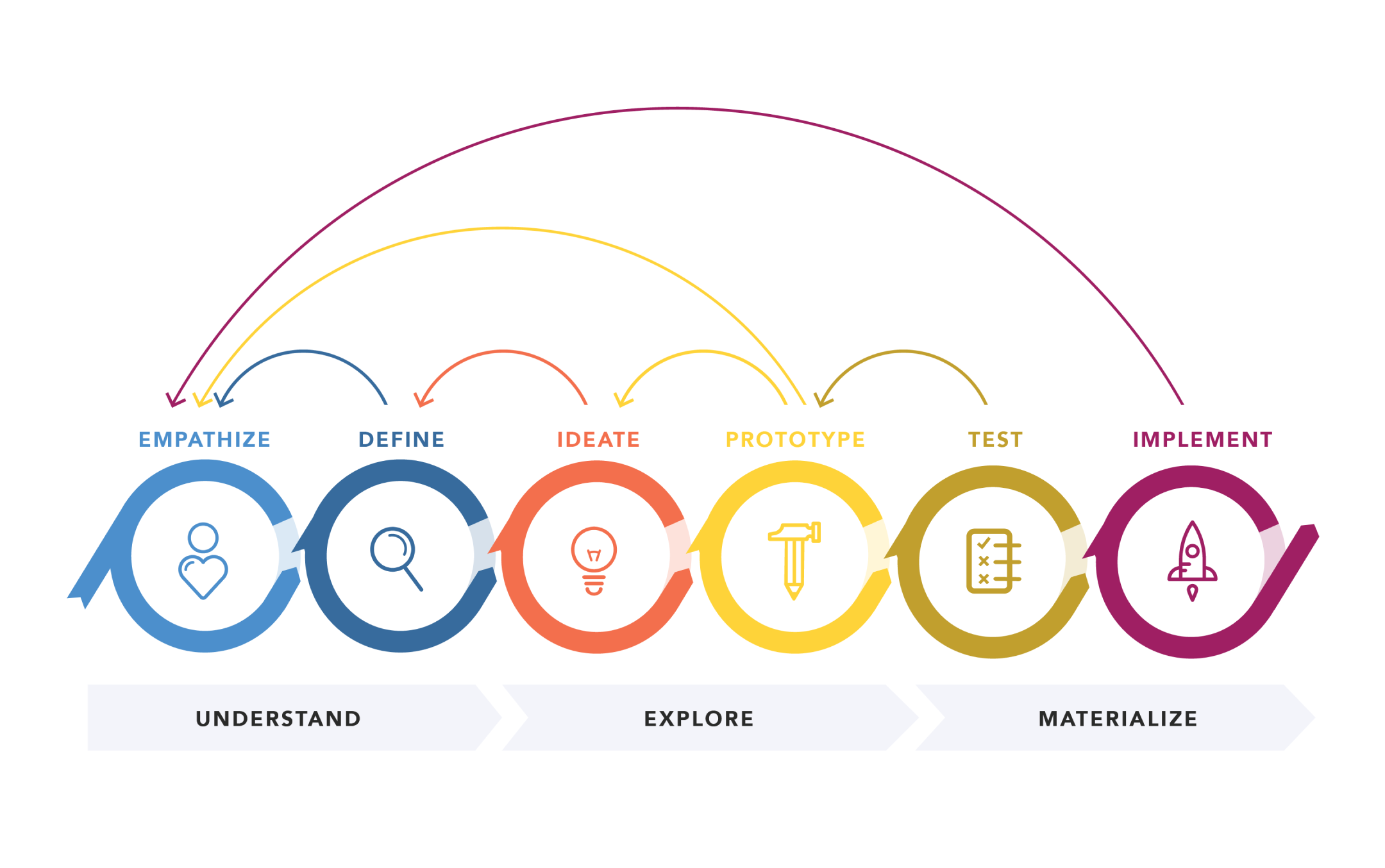

Solving Fragmented Liquidity in a High-Growth Market

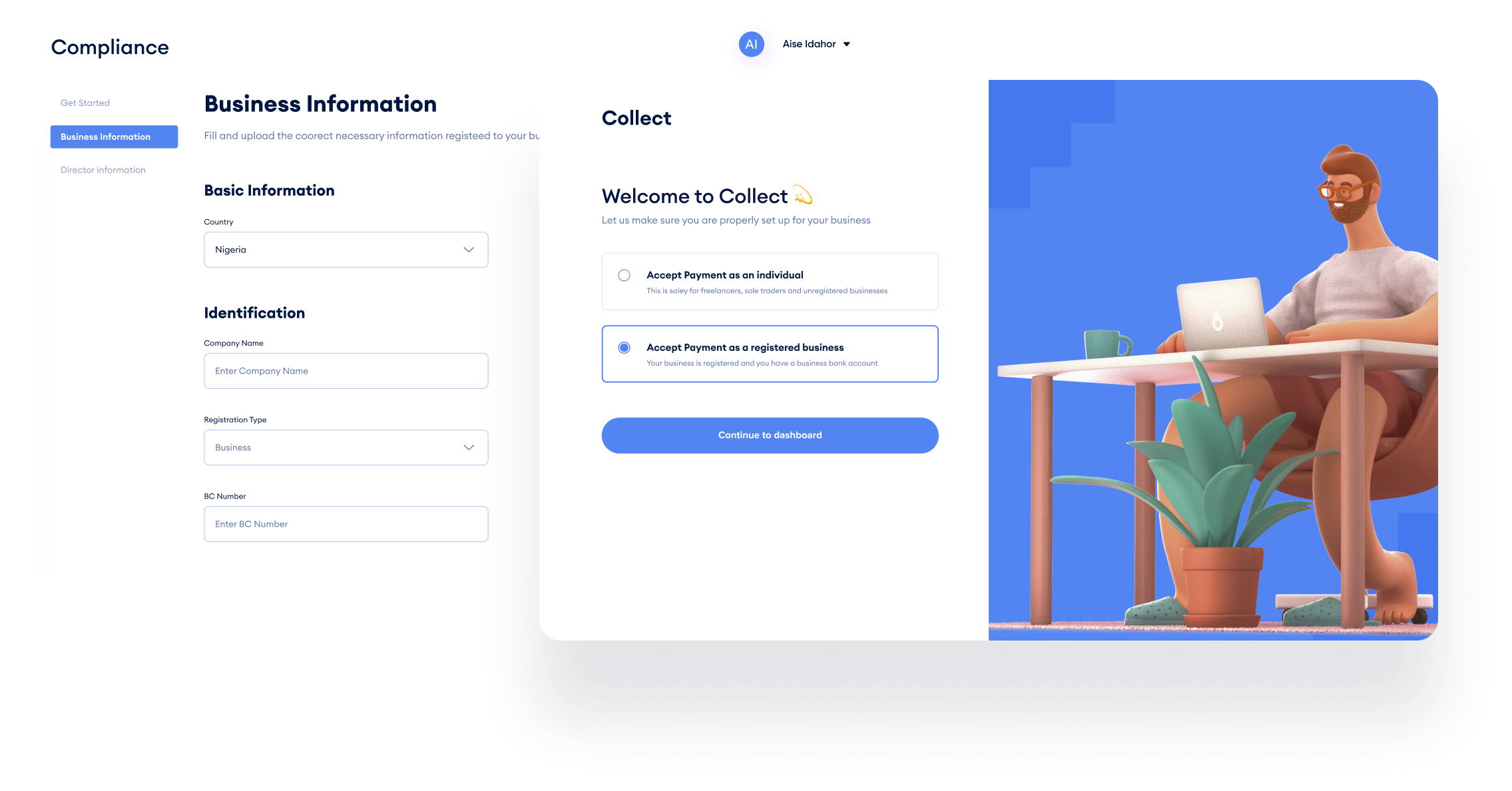

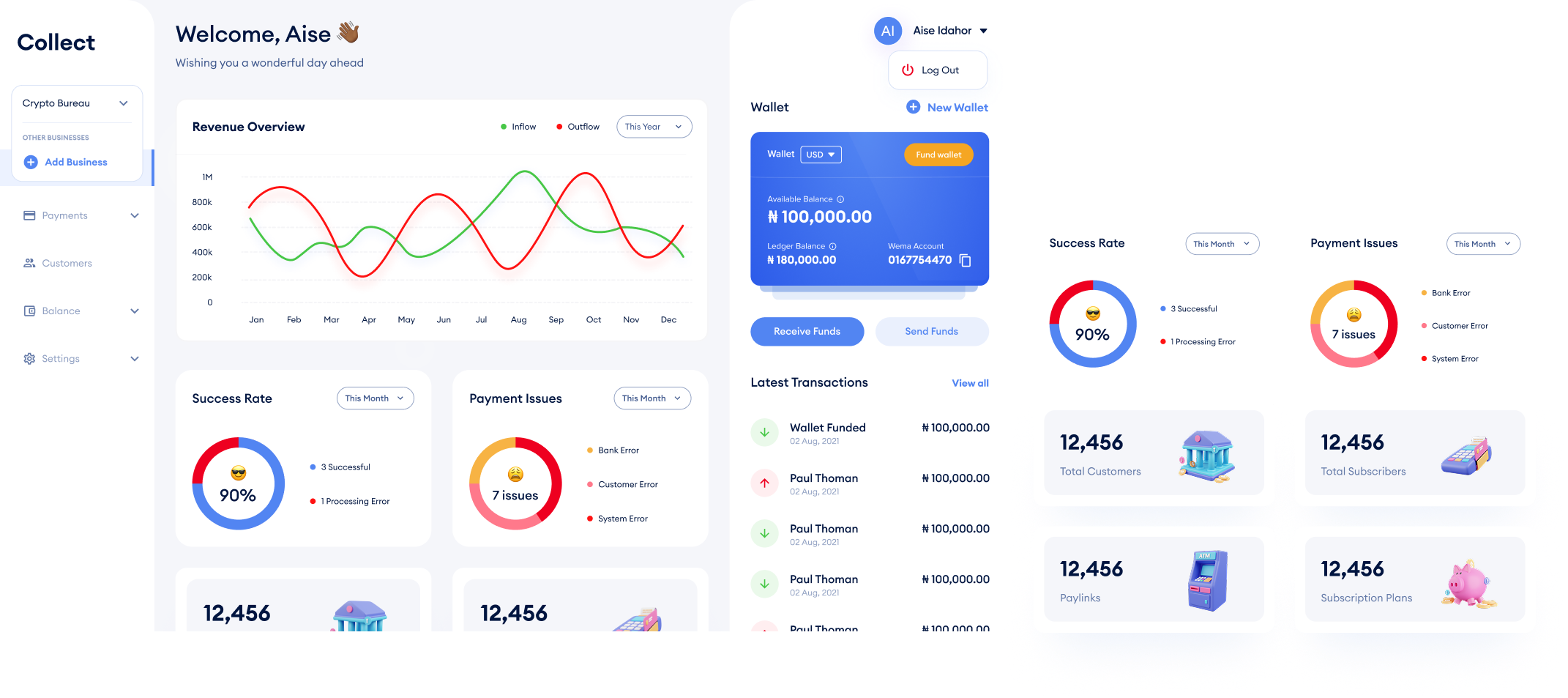

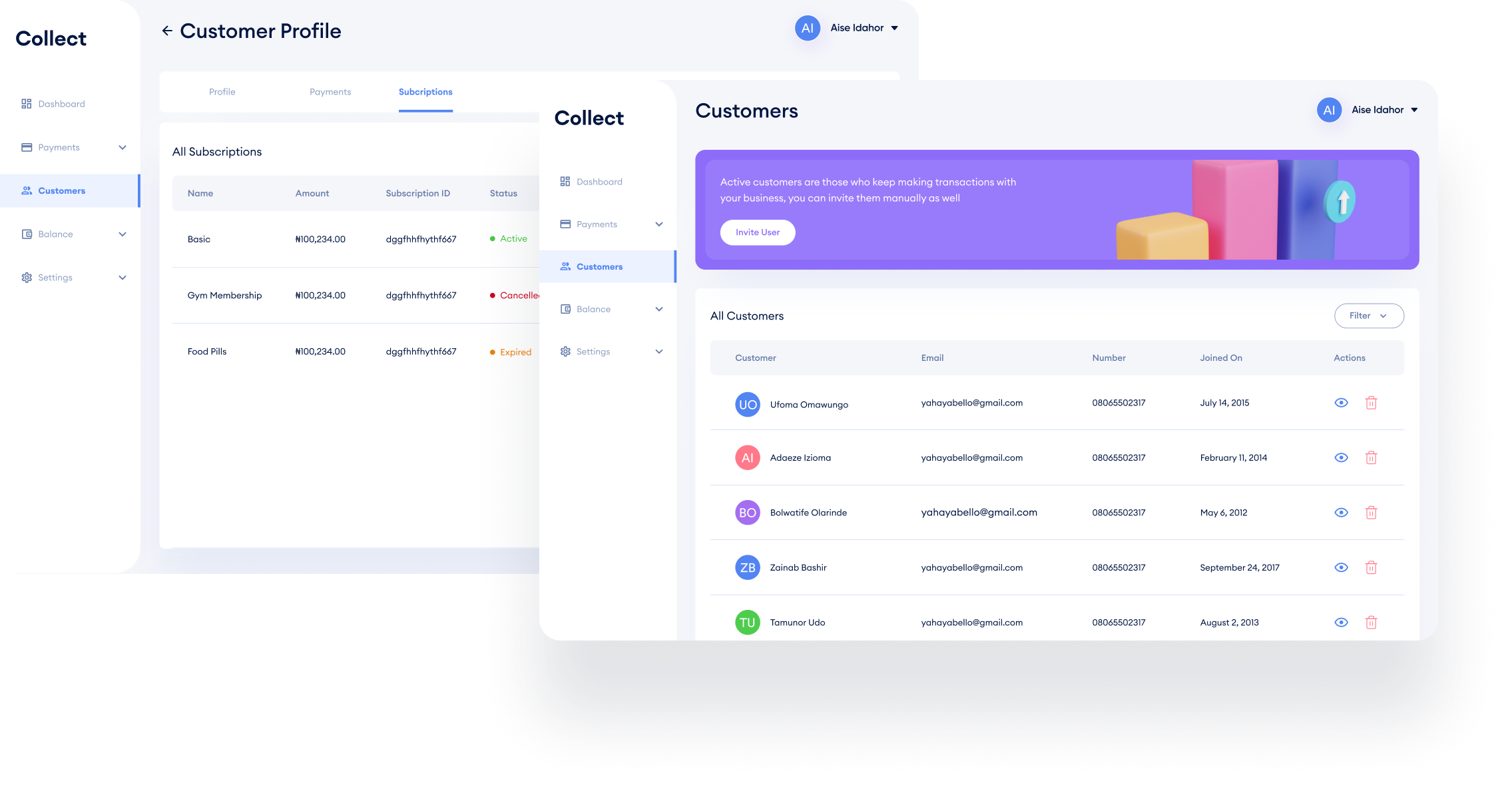

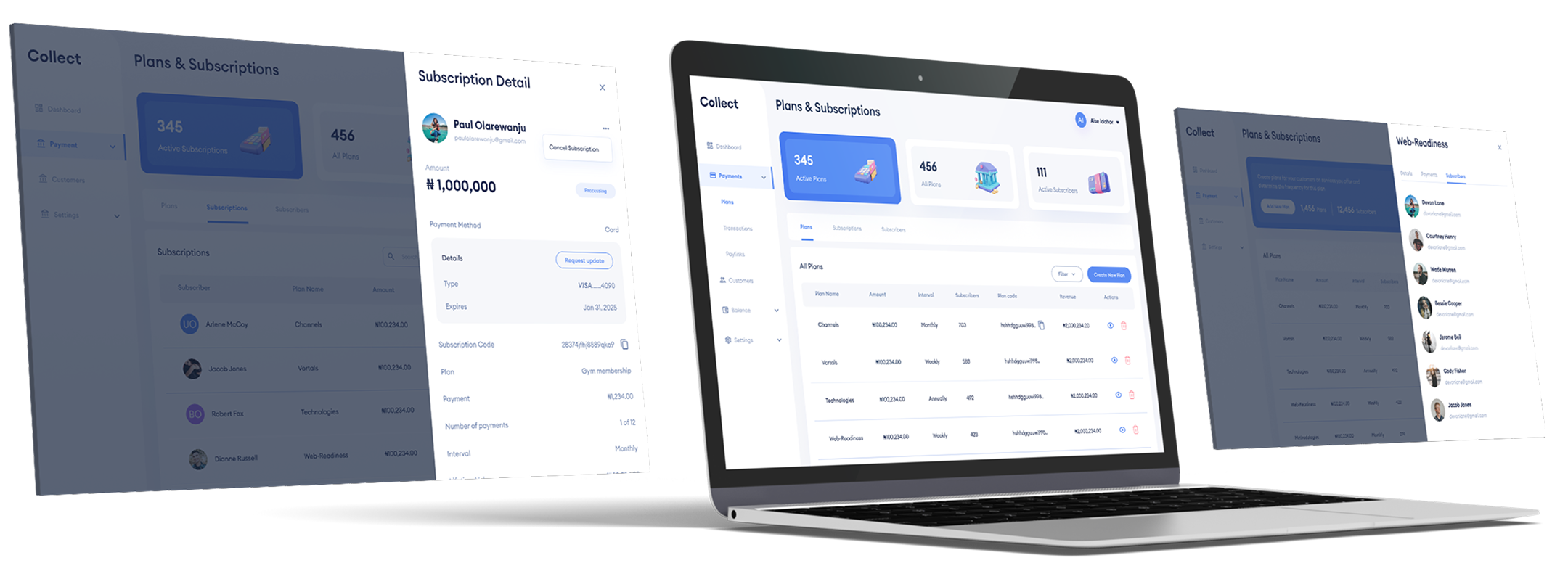

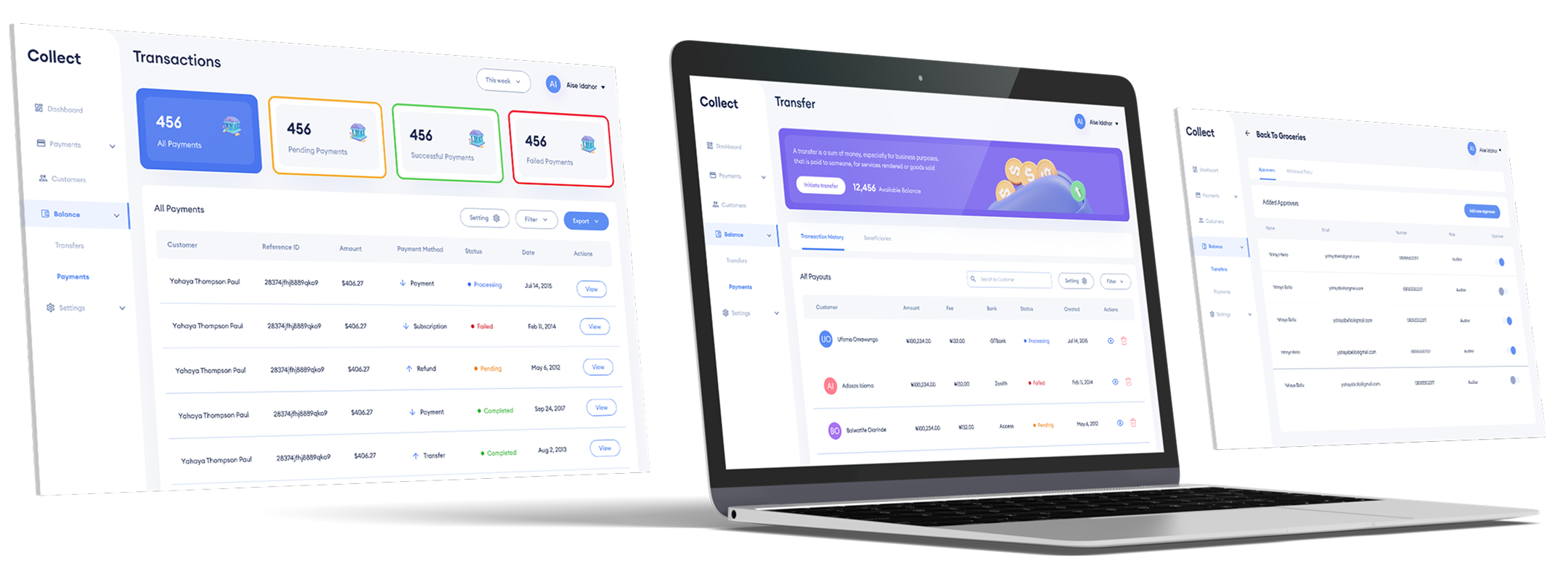

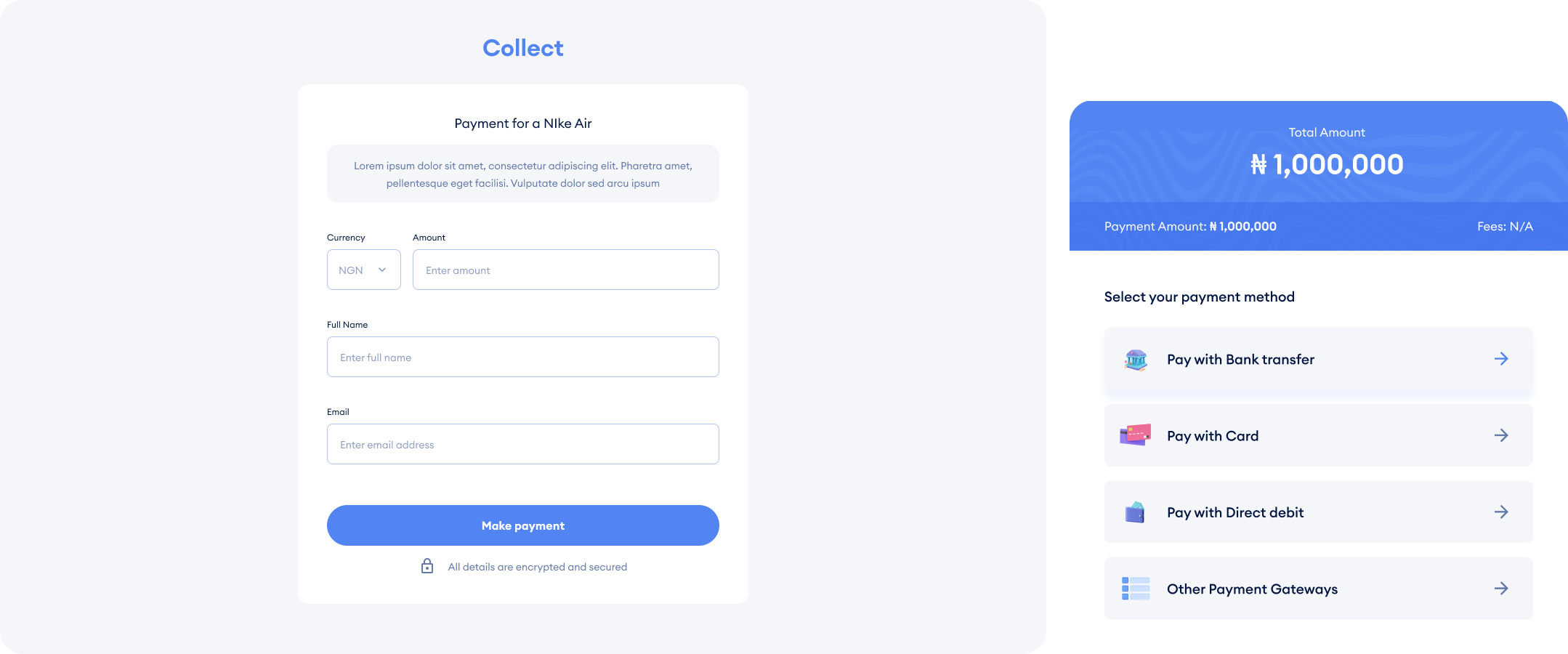

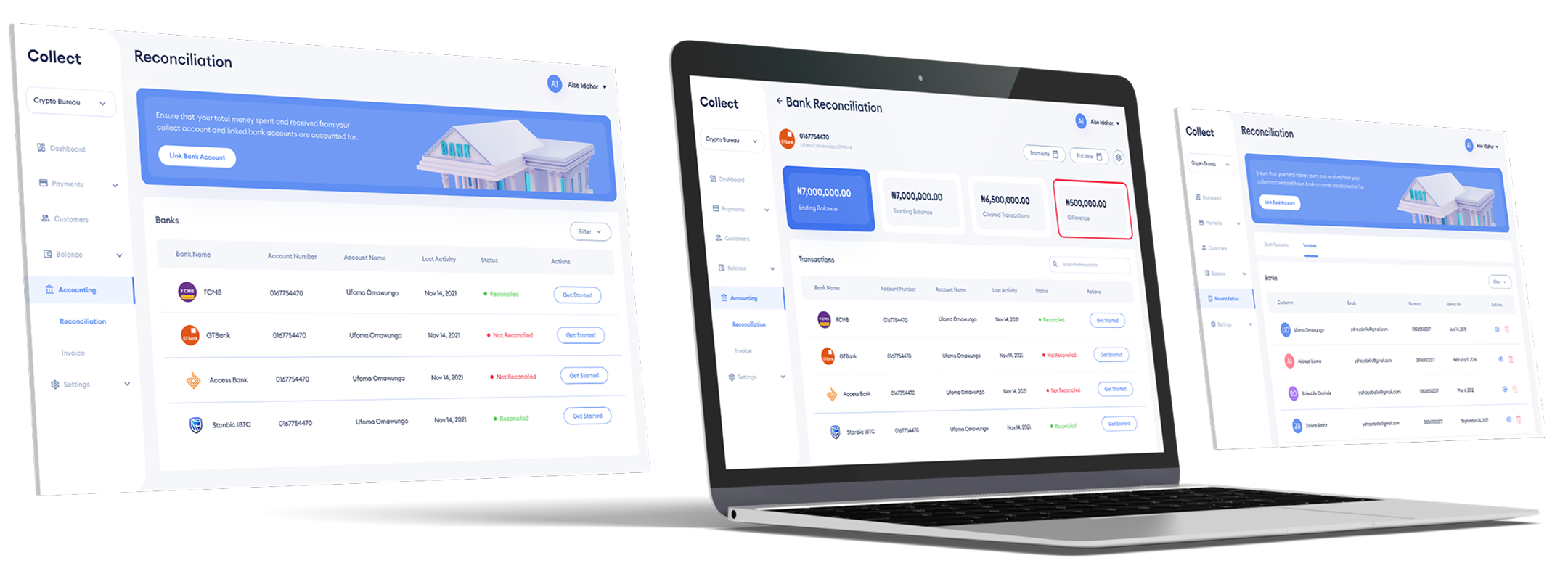

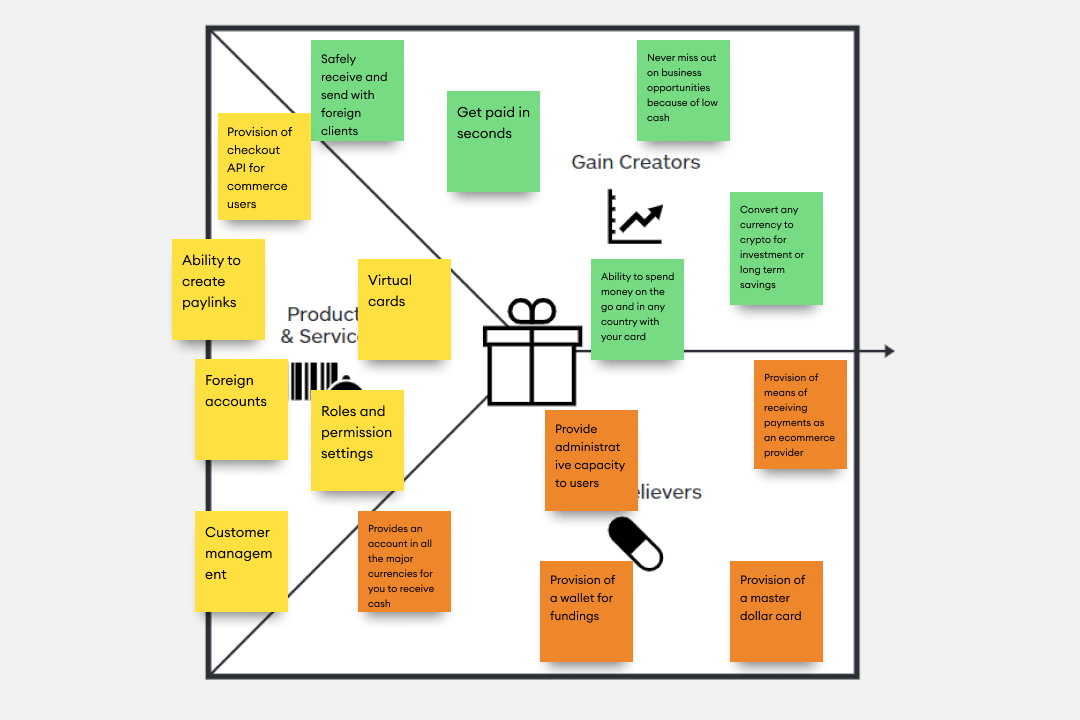

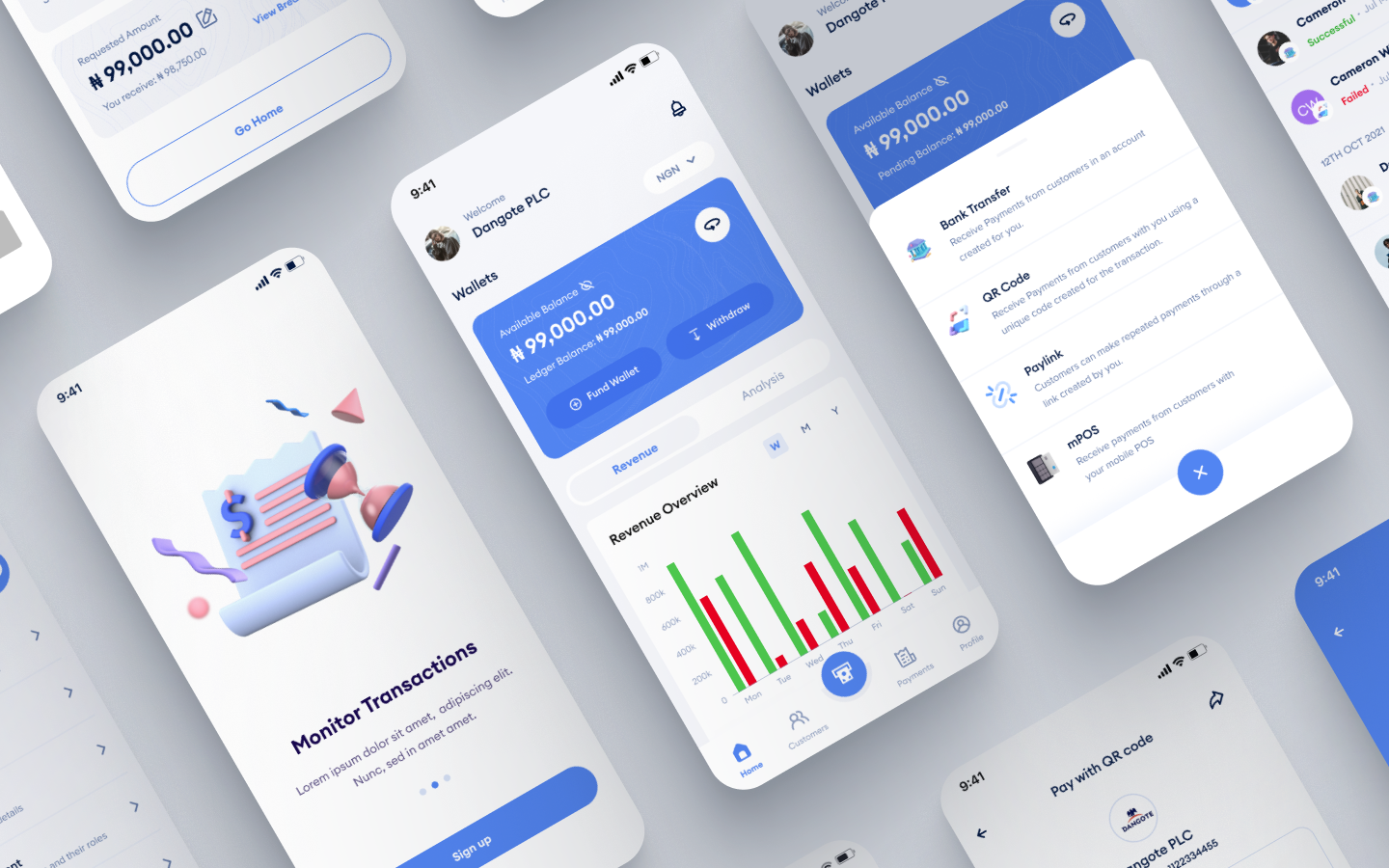

In a landscape of fragmented rails and manual reconciliation, Collect provides the infrastructure for businesses to scale. I led its evolution from a concept into a high-performance ecosystem, shifting the mental model toward unified financial orchestration. This framework bridges traditional commerce and digital standards, integrating multi-channel acceptance, bank transfers, POS, and online links, with automated tools for reconciliation and real-time capital management.

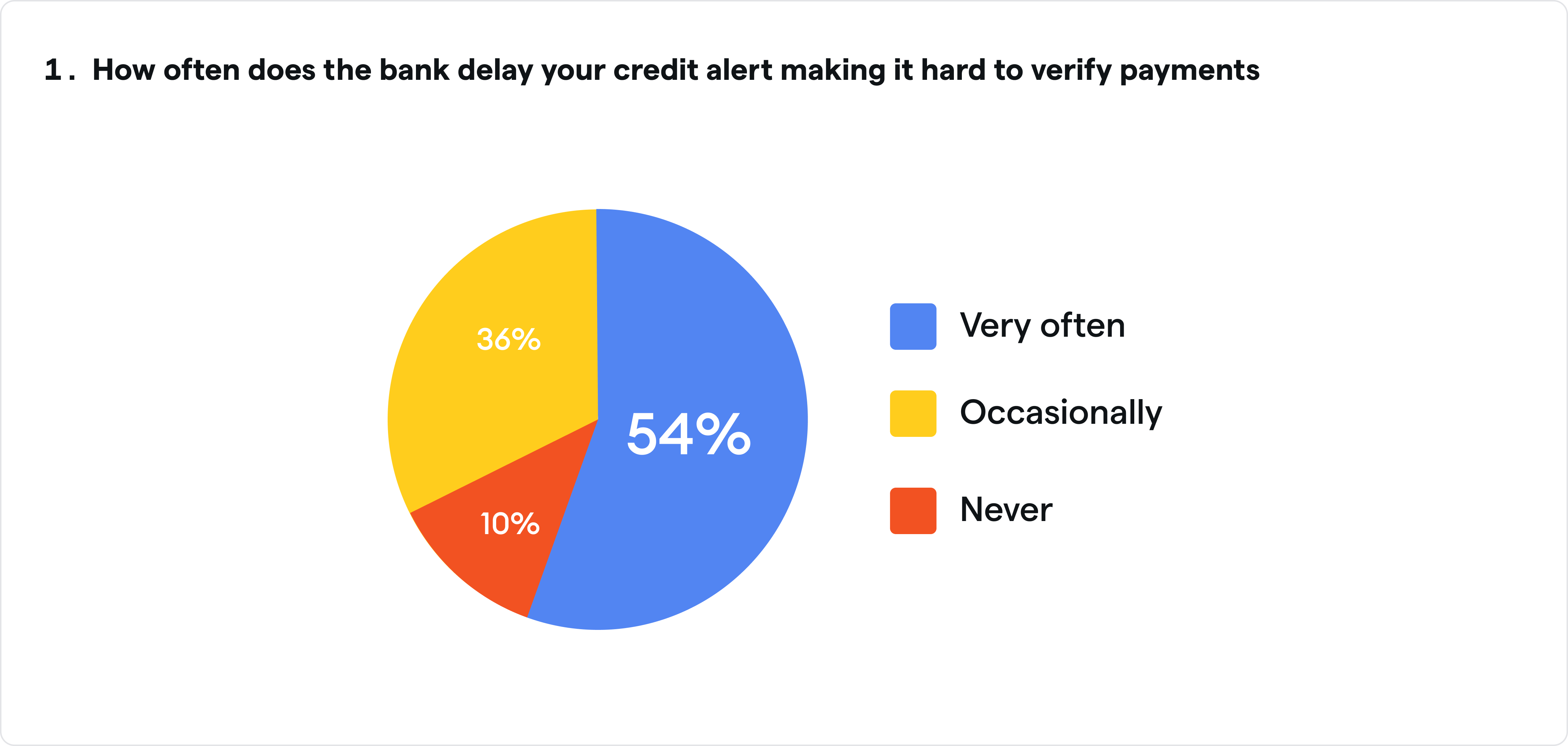

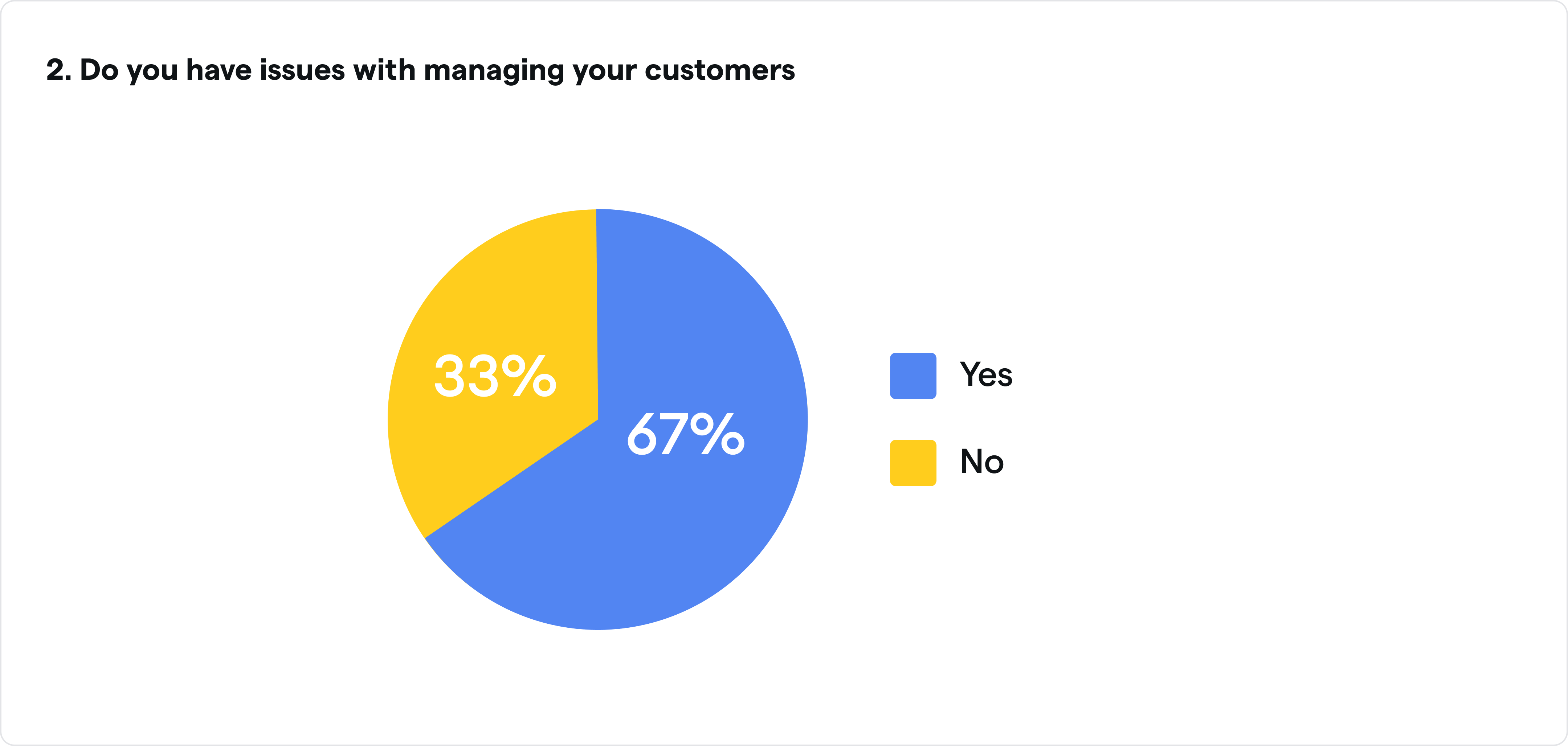

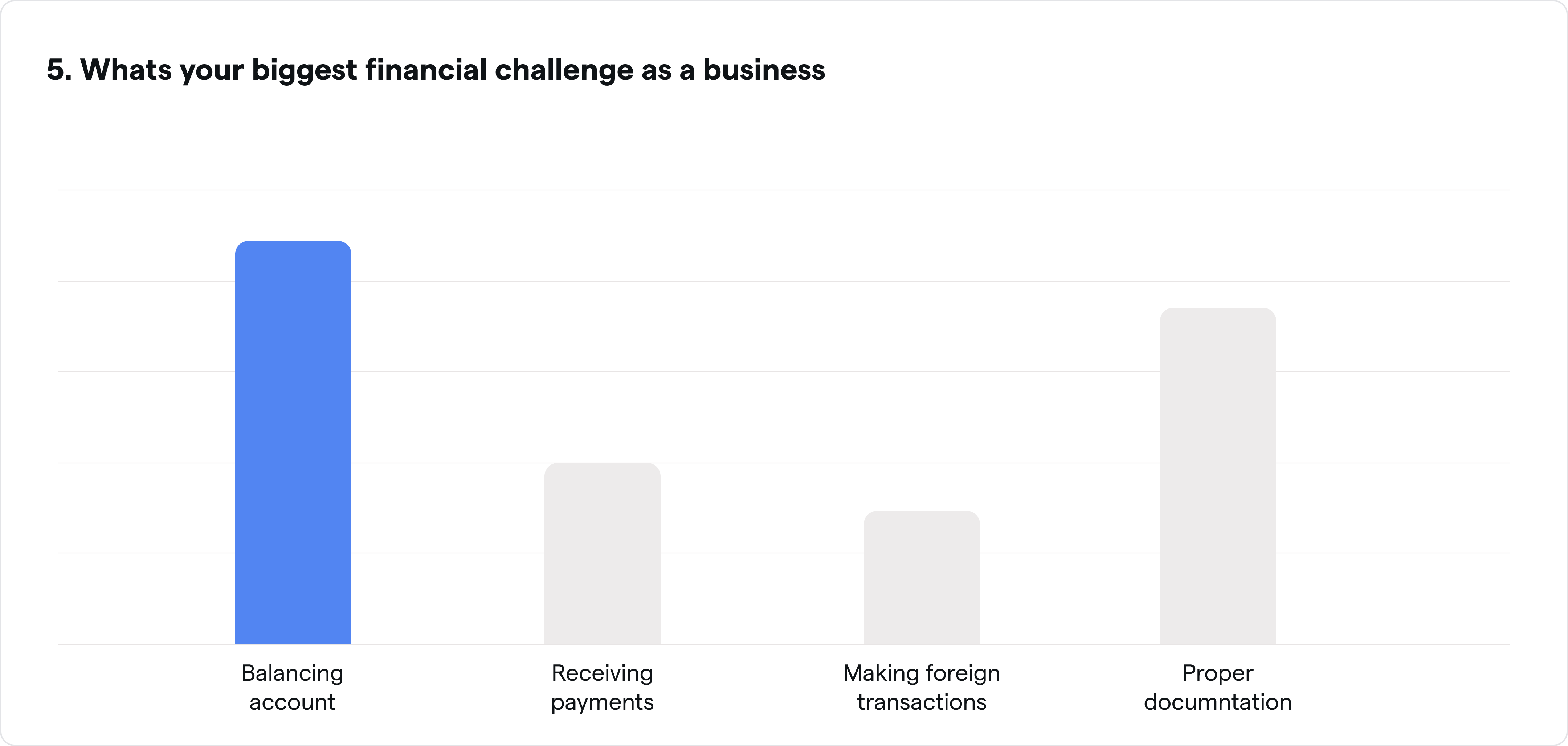

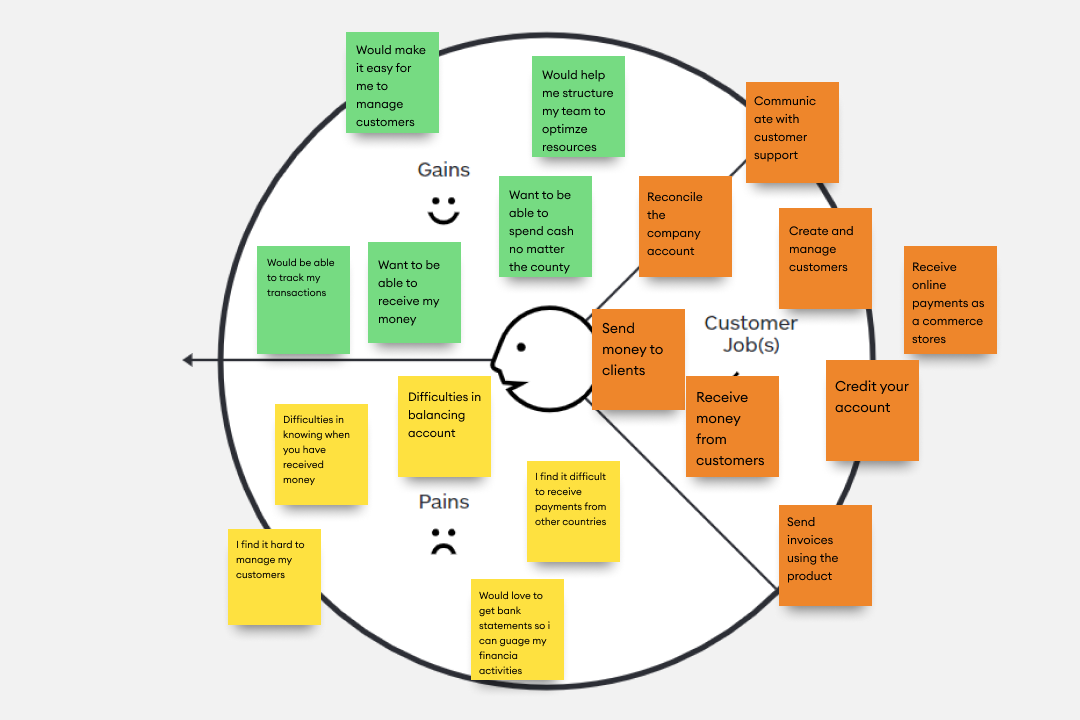

The Problem: Fragmented rails (too many ways to pay that don't talk to each other) and manual bottlenecks (auditing is a nightmare for these businesses).

The Constraints: Navigation of local regulatory shocks and technical integration hurdles (e.g., integrating multiple APIs like Mono and Okra to ensure uptime).

The Mental Model: Moving users from viewing payments as a "chore" to seeing them as a "growth lever" through unified data.

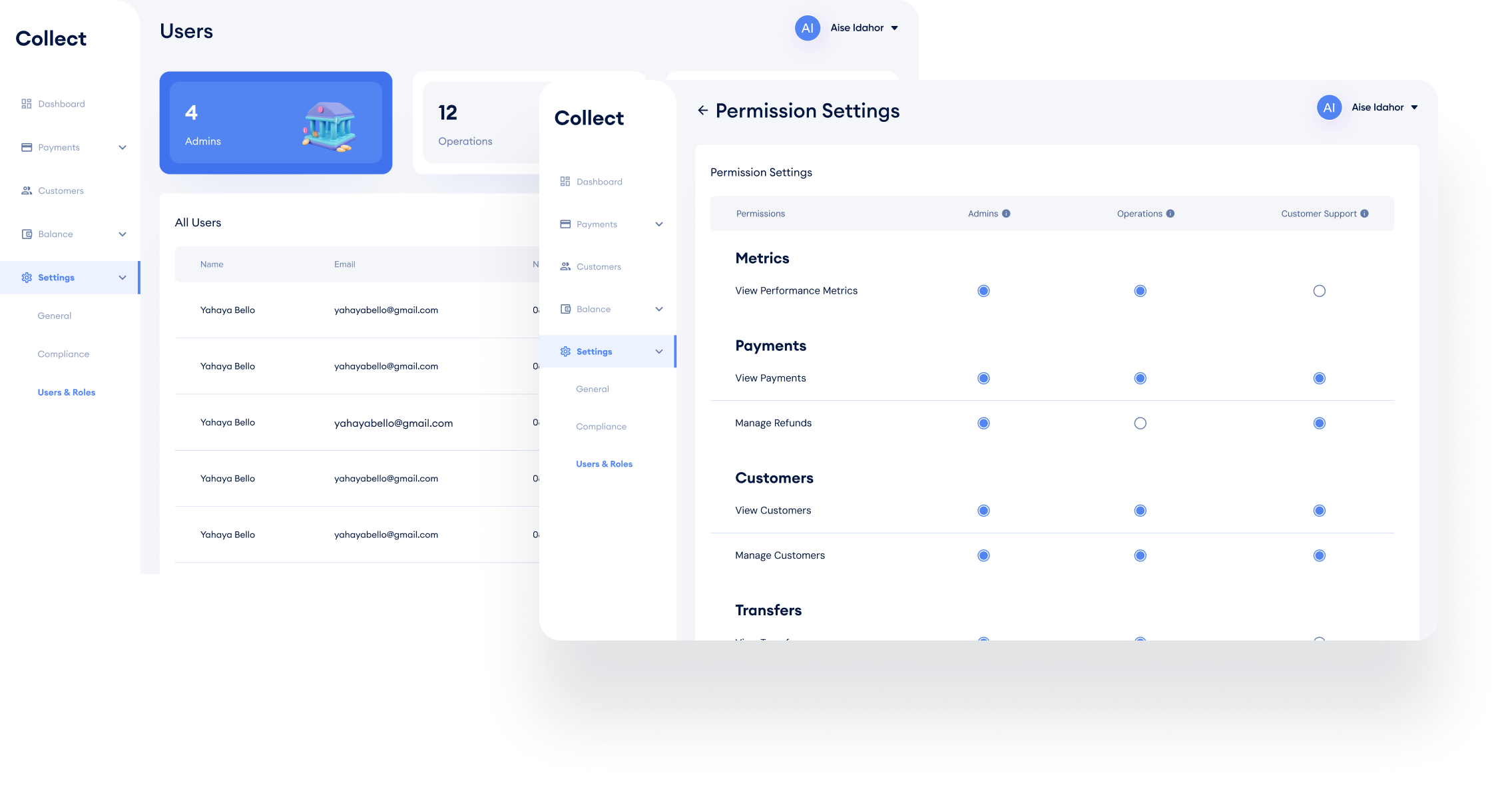

The Strategic Role: Your role in evolving the product from an idea (Direct Debit) into a full-suite "Financial OS".